Worldwide PC monitor shipments were slightly below 35.0 million units in the fourth quarter of 2013 (4Q13), a decrease of -0.4% compared to the previous quarter yet 2.9% more than forecast, according to the International Data Corporation (IDC) Worldwide Quarterly PC Monitor Tracker. The -3.8% year-over-year growth in 4Q13 was largely due to declining PC desktop sales.

"Dell and HP both saw increases in unit shipments for the worldwide PC monitor market for the second time in a down year," said Jennifer Song, Research Analyst, Worldwide Trackers at IDC. "At a regional level, EMEA experienced the largest positive growth during the fourth quarter, with Italy and Spain posting the biggest gains."

Looking ahead to the first quarter of 2014, IDC is forecasting a quarter-over-quarter decline of -9.0% in worldwide shipments to 31.7 million units. However, IDC slightly raised its total shipment forecast for the full year 2014 from 125.2 million units to 125.6 million units, which represents a decline of -8.6% compared to 2013. By 2018, worldwide shipments are expected to drop further to 104.8 million units, as the adoption of mobile devices at lower price points is expected to continue.

Technology Highlights

- LED backlight technology adoption continues to increase with 87.3% market share in 4Q13. This represents a year-over-year increase of 14.4 percentage points.

- Screen size of 21.x-inches wide has held the largest worldwide share for the last five quarters, with 20.7% share in 4Q13.

- Aspect ratio of 16:9 continues to dominate with 78.0% market share, which is more than 5 times the second most widely used aspect ratio of 16:10.

- Monitors with TV tuners are expected to grow to 7.9% market share by 2018, up from 5.4% share in 2013, led by LG and Samsung with a combined market share of 96% in this category.

- Touchscreen monitors are still a small segment of the total PC monitor market at 0.4% share, with sales mostly in the U.S. at 38.7% share. HP holds a 35.4% portion of the U.S. market.

Vendor Highlights

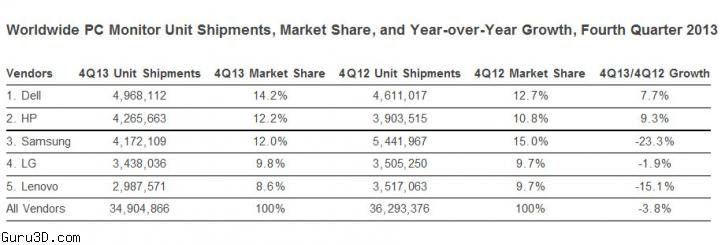

- Dell - Dell stayed in the number 1 position in 4Q13 with worldwide market share of 14.2% on shipments of 5.0 million units. While U.S. shipments declined -4.5% from the previous quarter, Western Europe and Asia/Pacfici (excluding Japan)(APeJ) delivered the biggest gains for Dell with 11.4% and 2.9% quarter-over-quarter growth, respectively.

- HP - HP rose in ranking to the number 2 position, with the largest quarter-over-quarter increase of 26.7% in EMEA. HP also saw positive growth in all regions this quarter.

- Samsung - Samsung remained third in unit shipments worldwide, yet maintains the top vendor in terms of total revenue with $1.08 billion in 4Q13, which represents 16.9% share in total market value.

- LG - LG maintained its number 4 position and continues to be the number 1 PC monitor vendor in Latin America with 28.4% share.

- Lenovo - Lenovo rejoined the Top 5 vendor ranking in 4Q13 after slipping to number 6 in the third quarter of 2013. Lenovo's biggest gains were in Western Europe and the U.S. with 17.7% and 9.1% quarter-over-quarter growth, respectively.